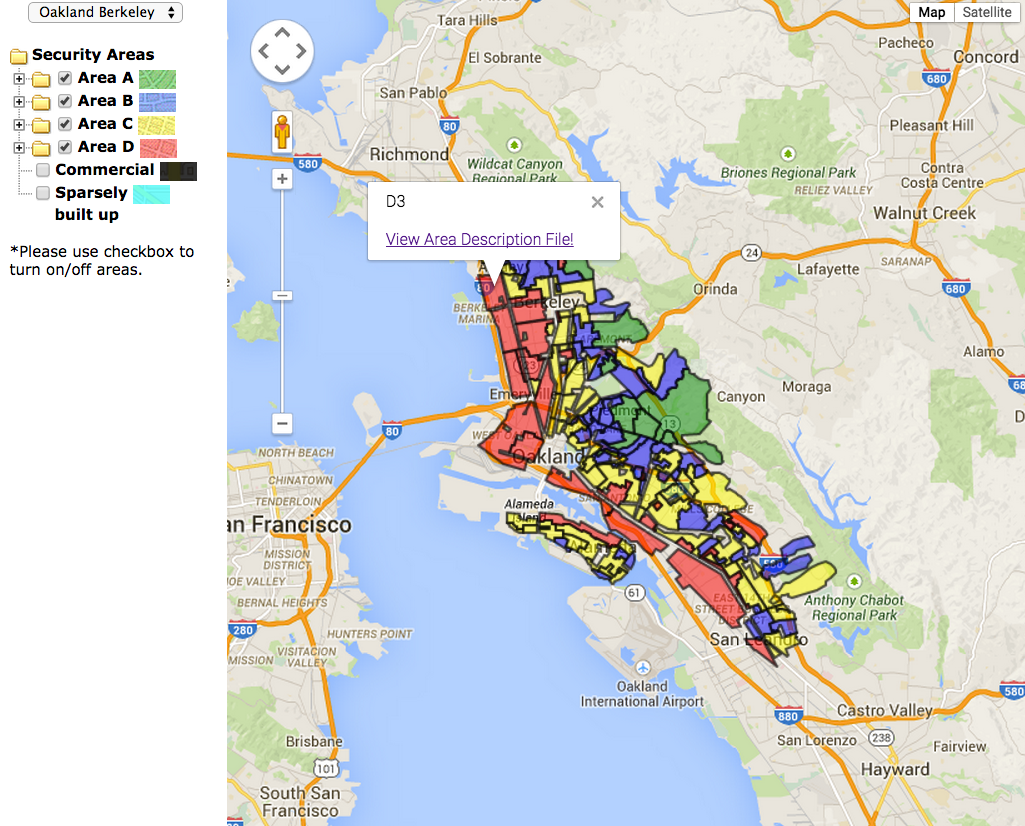

Richard Marciano (American, b.1962), University of Maryland (est. 1856), David Goldberg (South African, b.1952), University of California Humanities Research Institute (est. 1987), Chien-Yi Hou (Taiwanese, b. 1976), Rosemarie McKeon (American, b. 1957). T-RACES (Testbed for the Redlining Archives of California’s Exclusionary Spaces). 2010. AJAX, Apache 3.0, HTML 4.0, JavaScript 1.7, MySQL 5.0, and XML. Image courtesy the designers

T-RACES: Testbed for the Redlining Archives of California’s Exclusionary Spaces (Marciano, McKeon, Hou & Goldberg)

From the curators: T-RACES is a data visualization design that makes the history and effects of redlining newly tangible. Its focus is an interactive map that offers new access to archival documents from the National Home Owners’ Loan Corporation (HOLC). The federally sponsored HOLC was founded in 1933 to facilitate affordable mortgages as part of President Franklin D. Roosevelt’s New Deal response to the troubled economic climate in the aftermath of the Great Depression. The HOLC worked in tandem with local and national banks to assess real estate, basing the credit-worthiness of potential homeowners, in part, on their zip codes. The HOLC’s systematic discrimination against neighborhoods in which non-whites predominated was absolute–less than 2% of the $120 billion in real estate they financed between the 1930s and the 1968 passing of the Fair Housing Act was available to non-white families. Dialogue around this practice of redlining–termed so because of the red lines drawn on maps by banks and government institutions around areas where they practiced discriminatory lending practices–is not new. Scholars, activists, homeowners, and architects have highlighted this spatial and social violence for decades. The T-RACE team of researchers, a curator, and Web developers from the universities of Maryland and North Carolina at Chapel Hill have geotagged the HOLC archival documents. This gives scholars and the public alike stark new insight, at a very granular level, into the violence done to hopes and dreams of non-white homeowners through the practice of redlining. The repercussions still echo loudly today, as articulated powerfully in writer Ta-Nehisi Coates’s recent essay for The Atlantic, “The Case for Reparations.”

Enforced segregation by racial or ethnic origin and social status has a very old history. Not so long ago, slaves and servants occupied different spaces, oftentimes within the same household or estate. Violence was explicit and used to establish direct domination.

The advent of an industrial society and liberal democracy in Europe and the U.S. no doubt brought improvements to the conditions of minorities and the powerless. However, new forms of discrimination found their way around the formal public discourse of freedom and equality. Restrictive covenants made it all but impossible for minorities and immigrants to buy homes in specific neighborhoods. Yet, as decentralized mechanisms requiring coordination of all owners, covenants tended to achieve their intended segregating effect mostly in new subdivisions.

In the new American suburbs of the early 20th century, real estate developers could play an active role in establishing and coordinating “racial cartels.” However, it is hard to completely enforce segregation in an urbanized society of anonymous mobile citizens. Thus, the state came to the rescue of the established racialized notions of human nature that peoples of European origin fervently espoused prior to WWII. In the view of a “decent,” church-going, law-abiding white citizen, peoples of African descent were oftentimes seen as inferior, and immigrants often thought of as brutish, alcoholic, noisy, and quarrelsome.

Of course, overt population resettlement policies could not be implemented by elected governments in a society that wanted to see itself as fully democratic. Enter institutionalized redlining.

The housing mortgage is one of the greatest financial inventions, allowing non-wealthy families to access comfortable housing under a repayment schedule that suits their income levels. Mortgages have long been an instrumental facilitator of the “American Dream” of homeownership and comfortable living.

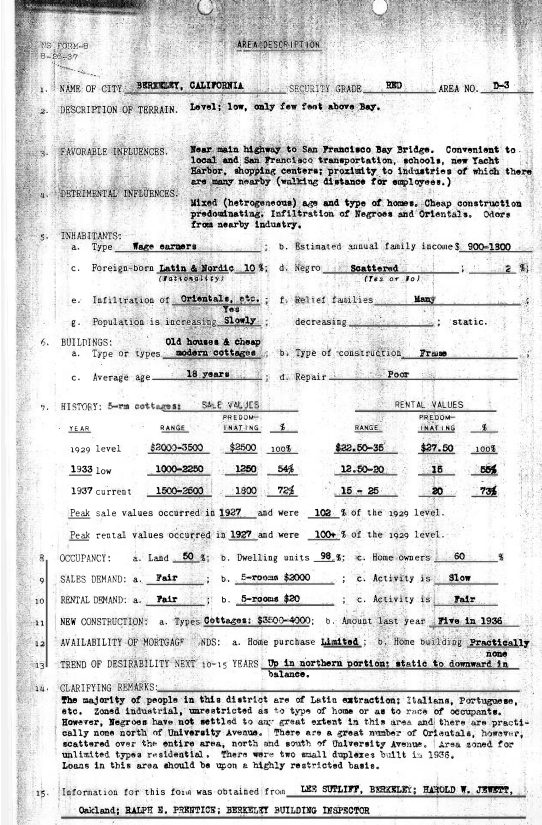

The T-RACES maps show how such a dream was turned into a nightmare for many families of African and foreign-born descent in the 1930s and beyond. Neighborhoods occupied by immigrants and minorities, or transitional mixed-income neighborhoods, were deemed “high risk” for lenders by the Home Owners Loan Corporation. This made it very hard for minorities to access loans, but also all but impossible for the white middle class to move into these neighborhoods, due to lack of credit. The language used in the maps and associated archival documents is violently demeaning and dehumanizing, including sentences such as “undesirable racial concentration,” “undesirables,” and “subservient racial elements.” These were sad times for humanism: across the Atlantic, fascist parties and the Nazis were infusing European intellectual thought with their notions of racial and national superiority.

In the U.S., redlining deeply affected housing markets. With poor access to credit, homeownership was harder in the neighborhoods designated as dangerous by the regulator. More importantly, this had a negative impact on housing prices in some of these neighborhoods: the lack of a stable source of financing made it very difficult for their neighbors to pay as much for housing. With declining housing prices, neighborhoods become imperiled. Often times, housing prices would go to a point below the replacement cost of the housing structures; no new development can be expected in neighborhoods where the price of a new home does not even cover its construction costs. Similarly, it does not make sense to invest large amounts of money in homes with very low market values: how can we expect a family to spend $15,000 on a roof on a house that may not be worth much more?

Therefore discriminatory institutional decisions had negative moral, social, and economic impacts on immigrants and minorities, but also deleterious physical impacts on their neighborhoods.

Acknowledging past wrongs and understanding the roots of current racial and economic segregation are very important to allow us to move forward. Another important lesson from these maps: the definition of violence should be construed by analyzing actual behavior—and perhaps intention—rather than by appealing to discrete, prescribed categories. Governments, markets, civil society, family structures, financial institutions, nongovernmental organizations, local communities, science, and the collection of current intellectual memes are all simply tools that can be used for alternate purposes. Social tools are only as good as their actual contemporary use.

The financial system can be used for bad purposes, but so too can governments, as the case of HOLC regulations sorely illustrates. It is the job of us all (institutions, architects and designers, scholars, homeowners, and beyond) to practically select all the tools at our disposal and change them or use them adroitly–in a humanistic fashion–to improve housing, economic, and social conditions for everyone.

January 7, 2017, 2:37 pm

Speck on Walkable Cities - But Who Will Walk Them? - Andrea Gibbons

[…] has been code for poor people, immigrants and people of colour since the 1930s and 40s with the federal governments’ Home Owners Loan Corporation and Real Estate industry guidelines that gave rise to redlining back when deeding your house to be […]

April 8, 2017, 1:00 am

Hosting

Tema foruma

T-RACES mashes up a popular commercial platform with public records housed at the National Archives in order to position digital material in a very particular way. Rather, the project brings these historical documents together with an informed body of scholarly research, creating the stage for important and timely investigations into the many ways in which the built landscape works in tight feedback loops with social attitudes about race.