Walid Raad: A few years ago, in November 2007 to be precise, I started a project on the history of the arts in the Arab world. I remember the month precisely because I had received a phone call around the same time from a woman whose name is November.

November calls me and asks me whether I'm interested in joining a retirement plan just for artists, something she called the Artist Pension Trust.

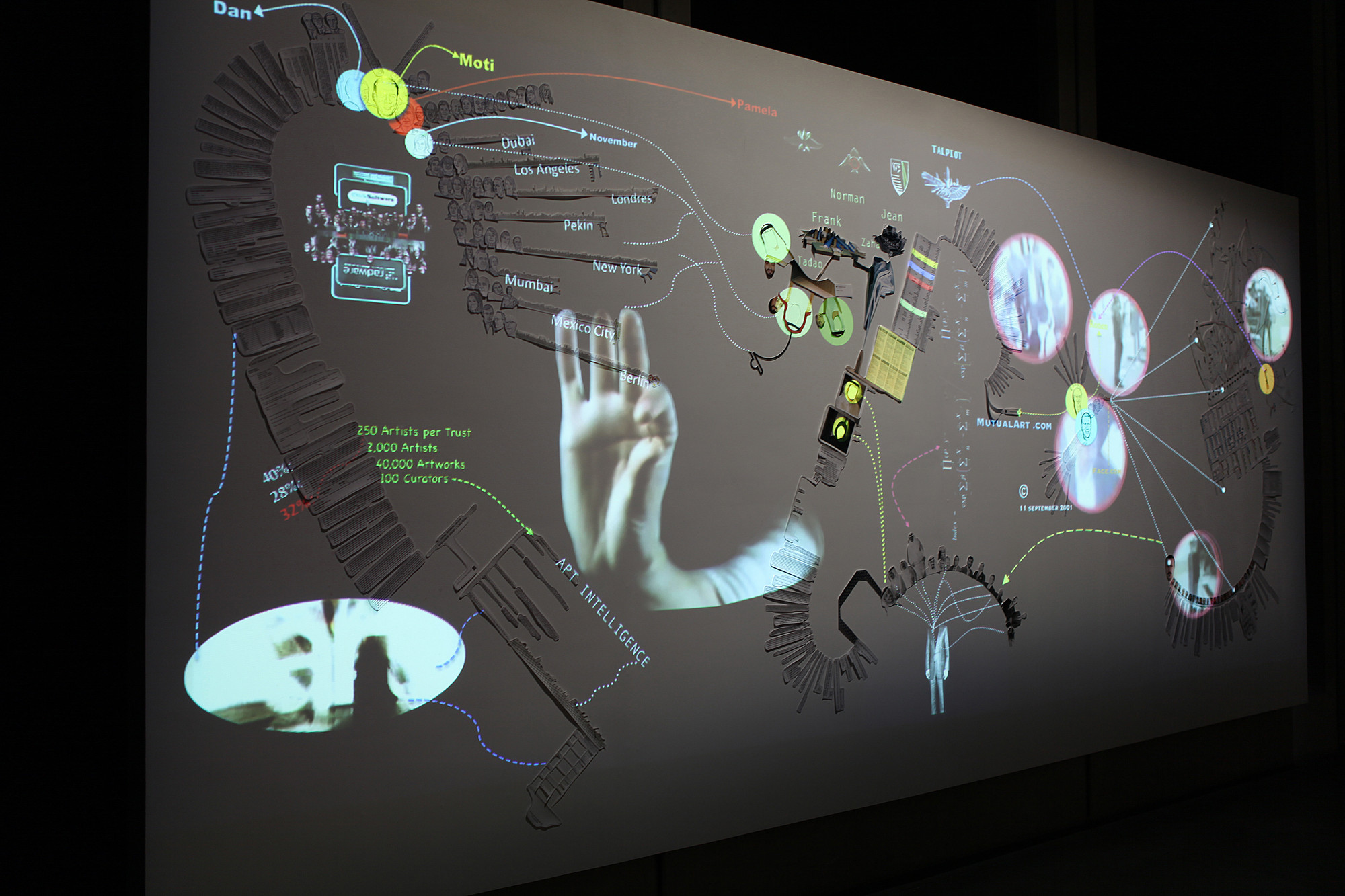

Now until that point, I had not even heard of retirement funds just for artists. And I had certainly not heard of the Artist Pension Trust. So I asked around, and I found out that the Artist Pension Trust—I will refer to it as "APT" from now on—I find out that the Artist Pension Trust was started in 2004 by two men. The first is a businessman, an entrepreneur whose name is Moti, or Mordechai Shniberg. And I soon found out that Moti had a partner, a man who came from the world of finance but not just any part of finance. He came from a particular area: the risk-management area. He was a sort of risk-management guru. His name is Dan Galai.

So how does this APT work? How did Shniberg and Galai structure this retirement fund just for artists?

The way they do it is that they usually go to a city where they know that a lot of artists live and work—Berlin, let's say for example. And once there, they contact a number of respected curators in that city. Then, they ask the curators to, in turn, contact up to 250 artists that the curators know and respect. The curators call the artists, maybe the way November called me, and they ask the artists if they want to join APT.

If an artist says yes, they're interested in APT, then the artist signs a contract with the company. And this contract binds the artist to donate to APT 20 artworks over the next 20 years. That's one artwork every year for 20 years.

When APT takes the works, it pays to store them. It insures them. It even preserves them. It may even lend them out to exhibitions who want to show the work. But by signing the contract, the artist has also given the company the option—the right to sell that artwork.

If and when APT decides to sell the artwork, 40% of the profits go back to the artist.

28% of the profits are taken by APT to pay for the storage, for the insurance, for the administrative costs.

And the remaining 32% of the profits—and this is what made APT very interesting to me, what made me think I should seriously think of joining them—the remaining 32%, it's always split, it's always divided, it's always shared. It's distributed among the 250 artists in each regional group.

This idea may seem simple, but it's actually quite interesting. It is interesting because Shniberg and Galai seem to have figured out something very basic about the commercial art world: namely, that this commercial art world tends to be very, very fickle. This means that an artist is usually hot critically—but more importantly from APT's perspective, commercially—for a very short period and cold for years or decades thereafter.

I read somewhere that the life of a contemporary artist in the art market today is around 40 months. This means that for 40 months you sell well, and then for months, years and even decades you're lucky to sell anything at all.

Today an artist who sells an artwork for $5,000 or $10,000 is usually not surprised if, in six or nine months, they cannot sell the same artwork for $500. Any artist who expects to make their living from the sale of their work in the market, we know this risk. We know it all too well. But it is this risk that Shniberg and Galai are trying to manage. And the way they're doing it is that by pooling artists into these groups of 250 potentially interesting artists—what they refer to as the "regional trust"—they figure that statistically speaking, it is more likely than not that two or three artists are going to be hot at any one time and selling well. And because 32% of the profits are always split, always divided among the 250 artists in the pool, this risk is minimized for everyone and every artist benefits.

This, it turns out, is a classic technique from the world of risk management—Galai's expertise. Shniberg and Galai are just applying this technique to the art world, that's all.

Today, APT has set up eight regional trusts. They have one in New York, Los Angeles, London, Berlin, Mumbai, Beijing, Mexico City. And then there was the trust I was asked to join, the Dubai trust.

And in a way, I was surprised that APT was starting this trust in Dubai because I did not know that in the Arab world and in 2007 we already had 250 interesting artists—or let me say, 250 artists who were selling enough work—that APT can build this kind of economy around them.

And I just wanted to know, who are the 250 artists? Because I just wanted to meet them, nothing more.

By 2012, APT had signed contracts with around 1,400 artists. And these artists had already given the company around 5,000 artworks. But if and when all the trusts close, which means if and when 250 artists join each trust, then APT will have around 2,000 artists under contract. And these artists will give the company in the following 20 years around 40,000 artworks, making APT the largest privately held art collection anywhere in the world—and this without the company spending a single dollar buying a single work of art.

I must admit, this is not bad.

Next to the retirement trust, Shniberg and Galai also set up a parallel structure, another unit they refer to as APTI: the Artist Pension Trust, the Intelligence unit. But this unit is not for artists; it's for curators. And here again, the idea is simple but fascinating.

Shniberg and Galai seem to have figured out that today there are not only individuals but, more importantly, there are large institutional investors—like banks, universities, pension funds, insurance companies—that are interested in buying artworks as an investment. But many are reluctant to do so because they know absolutely nothing about how the art market functions.

Let's imagine you're a pension state fund manager in—in New York, let's say, and you're interested in buying contemporary art from the Middle East to diversity your portfolio and because you keep hearing that this market consistently outperforms the S&P 500. Wouldn't it be interesting if you can go somewhere and actually talk to someone who knows a lot about this artwork and they can advise you on which artworks to buy, when to buy them, how much to pay for them, and when to sell them?

To set this up, Shniberg and Galai contacted over 100 curators. These are respected, renowned curators with expertise in different genres of art and in art from different parts of the world. So you're interested in art from Mexico. You contact APTI, and you ask them: "Do you have a curator who knows a lot about Mexican contemporary art?" They say, "Yes." They put you in touch with a curator. You meet with the curator. The first 10 minutes are always free to see if you get along, if you like their sensibility. And after this, every 30 minutes you sit with this curator, APT Intelligence charges you around $300.

And it turns out that many curators love this arrangement. This is understandable. Curators—these are people who are always talking to their friends, to their colleagues, about this interesting artist, this interesting artwork. But this information, they usually give it out for free. And now with APTI, finally someone is compensating them for their thus far uncompensated labor.

And institutional investors like this structure, too, because institutional investors do not necessarily trust commercial galleries. They think commercial galleries promote their artists only. With APTI, investors can actually talk to someone who is, to an extent, independent from the product traded.

And so with 100 curators, over 1,000 artists and 5,000 artworks, APT also actively promotes its collection by funding its own under-contract curators to produce exhibitions with their own under-contract artists and under-contract artworks. And as such, APT only manages to increase the value of curators, artists and artworks under contract.

Again, this is not bad.

It's now mid-2008, and I have yet to meet November. We've just been communicating over the phone and by email.

For some reason, I become quite interested in the man named Moti Shniberg, and I decide that I need to do some research to find out how Moti made his money. After a few Web searches over the course of a few weeks, I find out that Moti made a small fortune in the 1990s in an Israeli-based high-tech company called Image ID.

Image ID, it turns out, developed a system they call Visidot. And Visidot is a way to scan barcodes. But they don't do it with lasers; they do it with cameras. They do it optically. But this is not what I found interesting about Image ID.

The more I looked into Image ID—the more I looked at the investors, the employees—the more I find out that this company has a number of people who not only had served in the Israeli army—I mean, this is not a surprise, we all know quite well that in Israel most men and women have to serve in the army. Very few refuse, with grave consequences; but most end up serving. But with Image ID we have people who not only had served in the army, but these are people who had served in Israel's elite military intelligence units—these units right here, Unit 8200, Mamram and Lotem.

The link between APT, Image ID and Israel is already a problem for me for various reasons; but one of the problems is simply the fact that Israel and Lebanon are still in a state of war. And I'm not sure if you know this, but in Lebanon, any link between an Israeli person and a Lebanese person, a link between an Israeli institution and a Lebanese institution, will be trouble. And it does not matter if the Israelis you're associating with are progressive folks. They can be the most liberal, progressive folks in the world. They can support the Palestinian cause better than most Arabs. In Lebanon it does not matter. Any link will be trouble. But this is not just a link to Israel. I mean, do I want anyone in Lebanon to find out that I'm joining a retirement plan for artists started by an Israeli man who made a fortune in an Israeli-based high-tech company where most of the employees and investors have links to Israel's elite military intelligence units? This is no longer trouble. This is actually dangerous, and not just for me. This could be dangerous for any artist who joins APT. And I just wanted APT to be transparent about this. I just wanted the company to tell us whether this is true so we know what we're getting involved in, that's all.

A few weeks later, I take all this research to my first face-to-face meeting with November. And I had actually prepared three questions I wanted her to answer.

First, I wanted to know: Who is funding APT? Who are the investors?

I also wanted to know: Why is APT starting this Middle Eastern trust, the Dubai trust? Who are the 250 interesting Arab artists?

And I also wanted to know: Is there a real link between APT, Image ID, and Israeli intelligence, because at some point I started to think that I might have over-Googled Moti Shniberg and the links were not there, they were only in my head.

So I take the three questions to November and I asked them to her.

And she looks puzzled and embarrassed. Her face reddens, and she says she has no clue what I'm talking about. But she seems genuinely surprised and concerned by my questions and what they imply. She offers to put me in touch with her boss, a woman named Pamela.

A few weeks later I meet Pamela and ask her the same three questions: Where does the money come from? Why are you starting this Dubai trust? Is there a real link with military intelligence?

Pamela also has no clue, but she does not seem surprised by my questions because I think November told her, "You're going to meet this guy. He's going to ask you all these questions. Please be prepared." And to her credit, she's not only prepared. She actually asks me: "Walid, there's only one person who can answer these questions: Moti Shniberg. Are you interested in meeting Moti Shniberg?"

Am I interested in meeting Moti? Of course I'm interested in meeting Moti. I've been waiting for this meeting for the last 18 months. So Pamela sets up an appointment with Moti, and a few weeks later I find myself going to the APT headquarters. I think it was somewhere in Midtown, in Manhattan.

I enter a big loft space, around 25 meters long, 10 meters wide, a bit like this room. The receptionist welcomes me. She asks me to sit down for a few minutes before Moti comes out. Just before I sit down, I notice in the background 30 or 40 young men and women sitting behind laptops, earphones on, typing frenetically on their keyboards. It's a typical scene in today's high-tech world, so I don't really pay attention to it; but this will be important in a second.

I sit down, Moti comes out to greet me. I'm expecting Mr. Israeli Military Intelligence, and the man who comes out is simply the most beautiful man I have ever seen in my life. And at the same time, I'm thinking: Why did I ever think that military intelligence would not be beautiful to begin with? Moti is also impeccably dressed, clearly comfortable in his skin. He shakes my hand warmly, grabs me by the shoulder, takes me into his office. And then he begins to tell me how and why he started APT, and this is a clearly well rehearsed story. This is how it goes.

Moti is in a cab riding with an artist friend of his. He looks at her and asks her, what are her retirement plans. His artist friend says: "Moti, I'm an artist. Artists barely have any money. Do you think we have retirement plans?" He then asks her: "Why can't you invest your artwork like others invest their cash?" She looks at him and she says: "There is no such thing. I wish there was such a thing."

Moti gets out of the cab and he immediately calls his former finance professor, Dan Galai, and they come up with APT. Today they've already filed five patent applications on APT as an investment model.

Anytime I meet an Israeli, especially one around my age, we're going to talk about Palestine, one state/two states, divestment, sanctions. So we chit chat about Palestine. And then, of course, I begin with my questions. "Where does the money come from?" I ask Moti.

As soon as I ask my first question, it becomes very clear to me that Moti is not only beautiful, but he's very smooth and very, very smart. So when I ask my question—"Where does the money come from?," Moti looks at me and he simply says: "Well, Walid, you know, investors, these are people who prefer to remain anonymous. But I will tell you, and I will only tell you, that we have investors from the United Arab Emirates."

You understand what he's telling me. He's actually telling me: "Well, if you're freaking out because you think all the money is Israeli money, relax. Even Arabs are investing with me. And if Arabs are investing with me, why would you, as an Arab artist, mind working with me?"

And of course now I want to know: Who are the Emirati investors? But he's so smooth, and I'm so eager to get to my next question about the links with Israeli intelligence, that I don't even ask him any more about the Arab investors because I find myself gently pushed to ask my next question about the links between APT, Image ID and Israeli intelligence.

Keep in mind I've been researching this for the last 18 months. I've tracked every employee of Image ID. I know what other companies they've started. I know which units in the army they’d served in. I have proof right here in front of me.

As soon as I ask the question, something shifts. I can't tell if Moti's bored or upset. I can't read him anymore. He stays quiet for a few seconds, and then he says:

"You're from Lebanon, right? So, I'm sure you know how things are in Lebanon. I'm sure you know how things are in Syria, in Egypt, in Saudi Arabia. And I'm sure you know how things are in Israel. In Israel, many things are linked to the army. In Israel, the high-tech sector is always linked to military intelligence. Please don't tell me this actually surprises you. Please don't tell me you're one of those naive, left-wing, head-in-the-sand pontificators who actually think that the cultural, technological, financial and military sectors are not and have not always been intimately linked. Please tell me this is not who you are and what you think."

And of course, I am one of those—well, I would not say "naive pontificators"—but all of a sudden I don't want Moti to know this because it all seems so embarrassing, so callow. And I'm not ready to leave his office yet. I've waited two years for this meeting. I cannot just leave now. I have to find a way to stay in the office, so I just say to him: "Of course, Moti. Of course, you're absolutely right." And then I just look in the office. I gaze in the office, and I find myself asking: "Now, the 30 or 40 young people, the men and women, the kids with earphones on—what are they doing?" You see, I had not prepared this question. I just asked it because I needed to stay in the office. I needed to stay in the same room with Moti.

And as soon as I ask the question, Moti sits up. His demeanor changes. He smiles broadly, and then he says: "Okay, I can understand why you find APT interesting. But let me tell you what I find interesting." And then Moti begins to tell me about yet another company. And I'm sorry that I have to throw the name of yet another corporation at you. He begins to tell me about MutualArt.

MutualArt, it turns out, it's the parent company of APT. It owns all the regional APTs. It also owns the APT Intelligence unit. And later when I try to, of course, find out more about MutualArt, I can't, because the company is a BVI. That means it's registered in the British Virgin Islands, which means that the investors, the structure—they can remain secret.

Moti then tells me: "Well, MutualArt's biggest investment today, they're not the retirement funds. It's not the Intelligence unit. It's actually a website: MutualArt.com. Do you know the site?" Of course I know it. I use it all the time. It's a fantastic website. It's a website for anybody who loves the arts and wants to keep track of art matters in general. For example, you like the work of Francis Bacon. You sign into MutualArt.com and register the preference. You like Sophie Calle, you like Francis Alÿs, you like David Diao, you might even like my work—you do the same. And the site's algorithm is fantastic. It scans the Net and delivers articles, exhibitions, essays, catalogs that matter to you and only to you. Essentially, MutualArt.com is a database of its users' preferences.

Then Moti tells me: "Today, MutualArt has registered millions of preferences, and we are on our way to building the largest data set anywhere in the world about the art market. But this data set remains a noisy picture. And in order to turn it from a noisy picture into a clear picture with tendencies, clusters and nodes, we hired Ronen Feldman." Of course, of course they're going to hire Ronen Feldman.

After all, Feldman is the computer scientist. He's the man renowned for having coined the term "text analytics" in 1995. And of course I do more research on Ronen. And it turns out that he graduated from _the most celebrated_—I mean, take MIT, Harvard, Princeton, Yale and Caltech—add them all together, and you get this incredible unit in the Israeli army called Talpiot.

Anyways, Feldman's job is to write algorithms for large data sets. Take any large data set, filter it through a Feldman algorithm and all of a sudden, as if by magic, all kinds of tendencies, clusters and nodes begin to appear. And of course, these tendencies, clusters and nodes, they help you formulate questions and answers. And the questions that MutualArt was interested in are primarily about the art world—for example, auctions. When is the best time to buy or sell a painting by Andy Warhol: spring, summer, fall or winter? If in spring, is it better to sell in March, April or May? If in April, should one sell in the first half or the second half of the month, on Monday or Tuesday, at Sotheby's in London or Christie's in New York?

This is a question they've already answered, and the result: it's a financial instrument, a product that they're selling to institutional investors.

Then Moti tells me about other questions that MutualArt wants to answer, such as: How many articles written by what writers in what art magazines using what art language will affect the performance of an artwork coming up at auctions at the next Christie's?

And the last algorithm Moti tells me about, the one they were working on as I was meeting with him, was an algorithm about color. That's right, and more specifically about color in post-war European art. What percentage of blue, what percentage of red, what percentage of yellow, what percentage of black must a Picasso painting from 1946 contain in order to increase in value by 37% over the next 60 months? And as he's telling me this, I of course begin to see how the risk-management techniques of Dan Galai are now being combined with the text-mining expertise of Ronen Feldman in order to put in place—not in five years, but already to have put in place—complex, dynamic and real-time prognostic models about anything having to do with the art world.

And the more Moti is talking to me about MutualArt, the more he's talking to me about mathematical algorithms, risk management, semantic web-text analytics, Image ID, and the more I'm getting lost in all the details. And for some reason, I start to feel a bit tired. I'm feeling a bit nauseous, and I decided I needed some fresh air. I don't feel good all of a sudden. I decided that I needed to end the meeting. So I politely wind our conversation down and I thank Moti for his generosity and willingness to meet with me. I tell him that I need to go home and think about joining APT Dubai. To this day, I have not joined. I stand up, I shake his hand. I walk out of his office, go down the stairs. And I find myself on Fifth Avenue before I realize I forgot to ask him about the September 11 thing.

You see, I found out before my meeting with Moti was arranged that Moti tried to trademark the sentence "September 11, 2001." At first I thought it was a joke. So I do some research, and I find the court records. This is what they say: "USPTO—United States Patent and Trademark Office—records indicate that the application was transmitted electronically at 17:37 on September 11, 2001." At 5:37 on the afternoon of September 11, 2001.

The Towers, they go down at what time? 9:59 and 10:38. Six hours later, Moti is not just thinking. Moti has already filed an application to trademark the phrase "11 September, 2001." Six hours later, I'm still trying to get my emotions back in check, and this man has the amazing presence of mind, the masterful foresight to file to trademark the sentence "11 September, 2001." How do you train for this kind of presence?

But I don't ask him about this because—because I'm already a few blocks away. I don't want to go back. I'm a bit tired. I'm a bit nauseous. But more importantly, it's because I realized that I'm actually quite relaxed. When I secured the appointment with Moti, I thought that I was going to find all kinds of insidious links between collectors, artists, bankers, the military, Israeli intelligence, and financial wizards. I thought all these links would somehow be too much for me, that they would upset me, they would agitate me. But in fact, today, when I look at all of this, what can I say? Yes, I say to myself, this is intelligent. I would even say this is very, very intelligent. But at the end of the day, it is also all too familiar. It is all too banal. It is expected. And I for one, I for one don't find any of it insidious. I don't even find this interesting, certainly not interesting enough to deserve an artwork. After all, do we really need another artwork to show us, as if we didn't already know, that the cultural, financial, and military spheres are intimately linked? No, no we don't. This may be intelligent, but it is not insidious, and it is certainly undeserving of more of my words, so I'd better stop.

Five more minutes of historical facts, and then, I promise, other kinds of facts.

In the past decade or so, I've been very interested in how often I'm hearing about Arab art, whether it's contemporary or modern Arab art, about Islamic art, Middle Eastern art, its makers, its sponsors, consumers, its histories. But I've also been fascinated by the increasing number of festivals, museums, galleries, prizes, foundations that are emerging in cities like in Beirut, or Doha, or Cairo, Alexandria, Marrakesh.

But nothing is surprising me more than what is happening in a place called Abu Dhabi. As you may know, Abu Dhabi is one of the seven emirates that make up the United Arab Emirates, and Abu Dhabi is not only the capitol, Abu Dhabi is also the richest of the seven emirates.

Just to give you a sense of its wealth, today Abu Dhabi has between 3 and 5% of the world's proven natural gas reserves. It has between 6 and 9% of the world's proven oil reserves. At an average price of $100 a barrel, in 2012 Abu Dhabi netted around $120 billion from the sale of oil, and Abu Dhabi has been selling oil for a long time. So today, they're sitting on the largest cash reserves in the world. A sovereign wealth fund that's estimated to be between $700 and $800 billion that of course they invest. And the investment returns Abu Dhabi more cash every year than the cash they get from the combined sale of oil and gas. In other words, Abu Dhabi's not just rich. Abu Dhabi's very, very, very rich.

But Abu Dhabi also knows that the demand for oil is shrinking, and that its economy depends too much on this hydrocarbon dependence. So, in the past few decades, Abu Dhabi has tried to diversify its economy away from this dependence on oil, and it has invested heavily in other sectors. It has invested in aerospace, in healthcare, in biomedical technology, in education, in finance—and, as you may have heard—it has invested heavily in the arts and culture.

Their main investment in art and culture is the well-publicized Saadiyat Island, which means the Island of Happiness. This is a 27 square kilometer island—that's the size of Sicily. It's a $27 billion development project, and on this island today, Abu Dhabi's building the largest Guggenheim museum in the world, 45,000 square meters. It will be designed by the architect Frank Gehry. On the same island, right next to the Guggenheim, Abu Dhabi is building a Louvre, the Louvre Abu Dhabi, the Louvre that has not had a branch outside of Paris since 1793 will have a branch in Abu Dhabi. It's by the architect Jean Nouvel. Next to the Nouvel, they're building a performing arts center by Zaha Hadid. Next to Zaha Hadid, they're building a maritime museum by Tadao Ando. Next to Tadao Ondo, they're building a national museum by Fosters and Partner. Rafael Viñoly is designing a campus for NYU. And of course the island will have the marinas, the seven-star hotels, the golf courses—we know how these islands are built.

But it's also important to say that Abu Dhabi is not just hiring these starchitects to build them these cultural meccas that they will then fill with high-end art from the Middle East, North Africa, southeast Asia, in the hope that this alone will bring tourists by the millions, absolutely not. Next to the museums, Abu Dhabi is actually building colleges, universities, and art schools. But they're also setting up foundations, magazines, art journals, art prizes, art foundations, public and private collections. They're training art handlers, they're training insurers, and I even met somebody whose entire job is just to design Abu Dhabi's alternative art scene, because they figure all these students are coming to study at NYU, and students bring with them an alternative art scene, so wouldn't it be interesting to have an interesting alternative art scene in Abu Dhabi?

And of course when I hear this, all of this, for me as an artist, as an Arab, as an American, all of this is truly fascinating. I mean, how long have we been waiting, how long have I been waiting, for an Arab government to actually spend its wealth on art, on education, on healthcare and culture, and it's happening. It's happening today, and not just in Abu Dhabi. It’s happening in Qatar, it's happening in Saudi Arabia, and it's happening in Kuwait, among other places.

But then every time you ask the question, why are these Arabs all of a sudden so interested in culture, why are these sheiks and sheikas all of a sudden so invested in the arts, every time you ask this question, prepare yourself to hear two dominant and weighty caricatures that have emerged to make sense of all this.

The first caricature states that all this investment in the arts and culture in Abu Dhabi, it's a cynical move. It's a cynical move undertaken by a bunch of autocrats who are simply trying to diversify their economy away from hydrocarbon dependence onto tourism, all the while camouflaging, veiling their stay-in-power-longer, get-even-richer schemes under the civilizing cloak of culture.

In other words, these sheiks and sheikas in Abu Dhabi, they don't give a damn about the arts, they don't give a damn about the culture, they just care about more money and more power, and if they need a Louvre in the middle of their negotiations with the French for more French Mirages and military bases, so be it. What's a billion dollars for a Louvre? That's what the government of Abu Dhabi is paying the French government to license the Louvre brand for the next 30 years and six months—a billion dollars. What's a billion dollars for the government of Abu Dhabi? Remember that largest sovereign wealth fund I talked about, the $700 to $800 billion that they're investing? Every week it makes in interest a billion dollars. A billion dollars, it's Emirati pocket change. The French should've certainly asked more for their Louvre brand.

The second caricature says no, there's nothing cynical in all of this spending on the arts. In fact, it says, that all this investment in the arts and culture in Abu Dhabi, this is the sign of an Arab renaissance. This is the sign of young, new rulers seeking to assert the complexity, the diversity of Arab, Islamic, and Emirati values, especially after 9/11.

We're told this renaissance is led by Western-bred visionaries who are tired of the old ways. And who are wholeheartedly trying to first, democratize the taste of their citizens via the arts, and then, we're promised, they will democratize all aspects of civil and political life.

Yes, they may be licensing Western brands, like the Louvre and the Guggenheim, but we should give these leaders a break. We should give them a break for no other reason than they're actually doing things differently than their parents. I mean, weren't their parents spending all these petrol dollars buying more Ferraris and Bentleys than they could actually drive? Weren't they buying more apartments in London, Paris, and Tokyo than they will ever inhabit? And now, for a welcome change, these young visionaries are actually spending on healthcare, on education, on culture, and they're doing it at home. We should encourage them. We should support them, because they're only trying to do, after all, in 20 years, what it took the West 100 years to put in place.

I mean, after all, who built the Metropolitan Museum of Art in New York, who built the MoMA? Was it not society ladies, was it not robber barons? Let's call them American sheiks and sheikas. Was it not American sheiks and sheikas who established the Met over 100 years ago, and who helped shift the center of modern art from Paris to New York 70 years ago? Why can't Arab sheiks and sheikas do the same for Arab culture? They may not shift the center of contemporary art to the East, but they will surely establish an outpost for it there.

I must say, I don't know if these sheiks and sheikas are sincere, cynical, or enlightened. I have met some of them, and they seem to me like complex people, and like complex people, they make contradictory decisions, so they must be sincere, cynical, and enlightened at the same time. I don't know, and I don't think we will ever find out.

But there's one thing that I know for sure, one thing about which I'm absolutely certain.